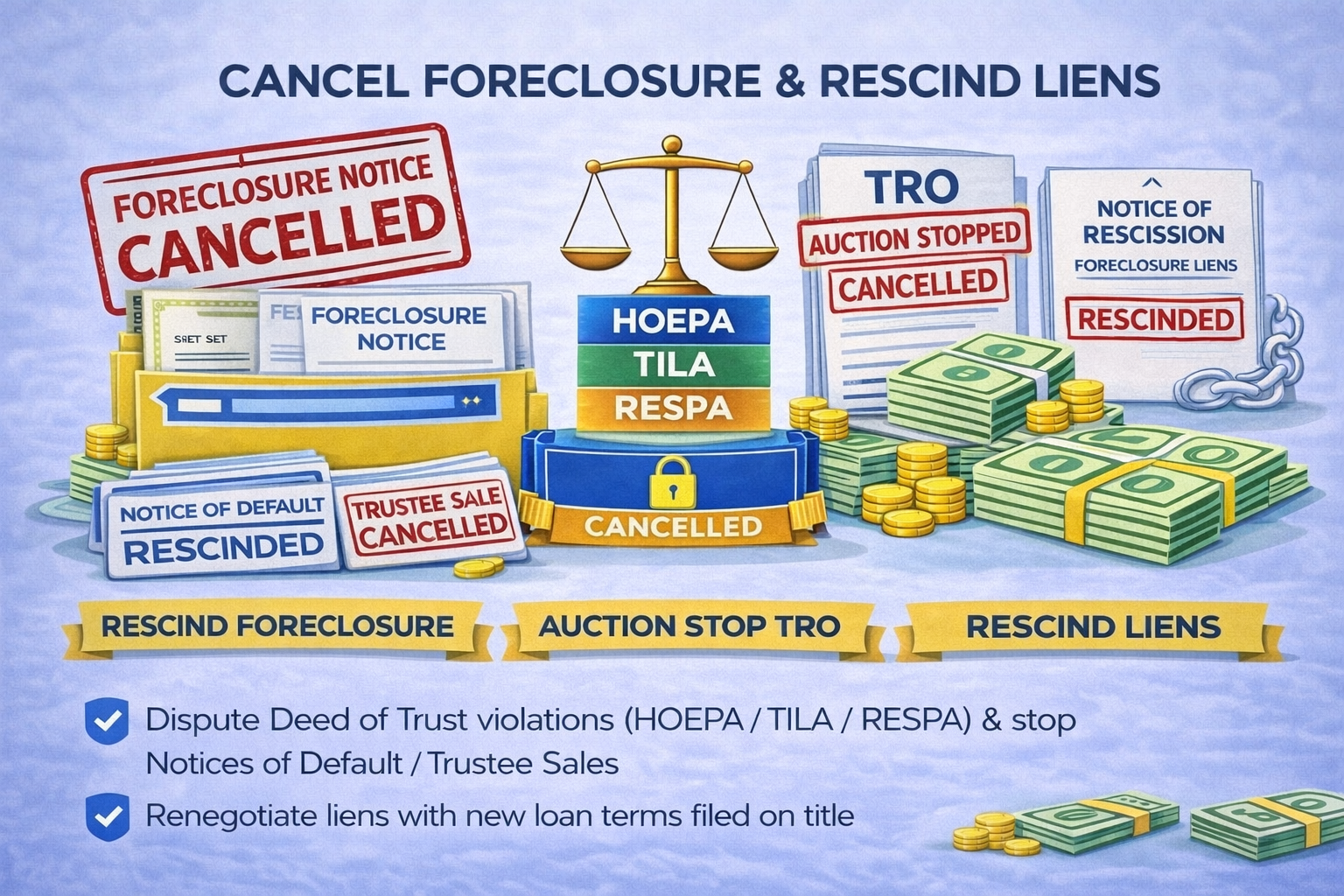

Cancel Foreclosure & Rescind Liens —

Stopping Foreclosure and Clearing Default Notices Through Legal Compliance Review

When a homeowner receives a Notice of Default (NOD) or Notice of Trustee Sale (NTS), the foreclosure clock begins to move quickly. But lenders and servicers must follow strict federal and state laws when handling mortgages, disclosures, and foreclosure procedures. When they fail to comply, homeowners gain powerful leverage to pause foreclosure, dispute errors, and renegotiate loan terms.

Dream Financial Management helps homeowners identify servicing violations, challenge improper foreclosure actions, and work toward rescinding liens, canceling foreclosure notices, and resetting the loan under new, affordable terms.

How We Help Stop Foreclosure Immediately

Our foreclosure‑defense strategy focuses on identifying violations, disputing errors, and using consumer‑protection laws to halt the foreclosure process. This may include:

Challenging inaccurate or incomplete disclosures

Disputing improper servicing practices

Requesting a full accounting and validation of the debt

Filing disputes that require the servicer to pause foreclosure activity

Using legal compliance findings to negotiate new loan terms

When errors or violations are identified, lenders are often required to cancel the Notice of Default, rescind the Notice of Trustee Sale, and restart the review process, giving homeowners the time and leverage needed to save their home.

Consumer Protection Laws That Strengthen Your Case

We help homeowners assert their rights under major federal mortgage‑protection laws, including:

TILA (Truth in Lending Act) — Ensures accurate disclosures, interest calculations, and loan terms

RESPA (Real Estate Settlement Procedures Act) — Regulates servicing practices, escrow handling, and error‑resolution procedures

HOEPA (Home Ownership and Equity Protection Act) — Protects borrowers from predatory lending and abusive loan terms

When servicers violate these laws, foreclosure actions can be paused or reversed until the issues are corrected.

Using Violations to Renegotiate Your Loan

Once foreclosure activity is stopped, Dream Financial Management works to negotiate a new, affordable loan structure. This may include:

Lowering the principal balance

Reducing the interest rate

Securing a new 30‑ or 40‑year term

Lowering the monthly payment

Resetting the loan on title as a new agreement

Removing all foreclosure‑related liens and notices

This approach not only saves the home but also creates long‑term financial stability for the homeowner.

Our Process for Cancelling Foreclosure & Rescinding Liens

Dream Financial Management handles the entire process from start to finish:

Reviewing all foreclosure notices and loan documents

Identifying servicing violations and compliance errors

Filing formal disputes and error‑resolution requests

Demanding a pause in foreclosure activity

Working with the lender to rescind NOD/NTS filings

Negotiating new loan terms based on compliance findings

Ensuring all liens and foreclosure notices are removed from title

Our goal is to protect your home, restore your rights, and secure a sustainable mortgage solution.

A Second Chance to Save Your Home

Foreclosure does not have to be the end. When lenders fail to follow the law, homeowners have powerful tools to stop the process, clear their record, and rebuild. Dream Financial Management stands by your side to challenge improper actions and negotiate a fresh start.